By Monica G. Ng’aru

Overview of the African Market

In the majority of African countries, more than 70% of health technology requirements are imported and over 90% of the medical devices in public hospitals are imported. This situation is untenable both now, and in the long run. The advent of the COVID-19 pandemic accelerated the urgency and agency for African governments to seriously consider investing in localization of medical health technology manufacturing (drugs, vaccines, medical devices, and diagnostics). Covid-19 demonstrated that the current African health-industry complex, comprising of local health industrial structures, value chains, and supply chains, and other supporting industries was woefully unprepared to rapidly address fast-moving public health emergencies.

The African Medical Devices market size was valued at US$ 4.2Bn in 2022 and projected to grow from US$ 4.49Bn in 2023 to US$ 7.786Bn by 2032 exhibiting a CAGR of 7.1%. The African market has a rapidly growing population and an increasing burden of diseases, making it a potentially lucrative market for medical device manufacturers and suppliers. However, it also faces infrastructure, regulatory, and economic challenges.

The market segmentation based on end-users include Hospitals, Ambulatory and Home. The hospitals segment generates the most income because there are more community hospitals and clinics on the rise to cover the demand for better healthcare within the rising African population. Factors like rising government efforts, increased R&D activities and a rise in regional market participants drive the market for medical devices. Manufacturing locally is one of the cost-cutting strategies used by manufacturers in Africa to remain competitive from a price point in competition with international players in the market. Major players in the medical devices market attempting to increase market demand are investing in R&D operations include Medtronic, Stryker, Johnson and Johnson Services Inc., F. Hoffmann-La Roche Ltd, Mindray Medical International Ltd., Koninklijke Philips Electronics, Siemens Ltd., Toshiba Medical Systems Corporation and GE Healthcare.

Kenyan Market Outlook

Kenya has a market-based economy and is generally considered the economic, commercial, financial and logistics hub of East Africa. With the strongest industrial base in East Africa, Kenya has been successful in attracting exporters and investors around the world. In 2019, Kenya was named one of the fastest growing economies in Sub-Saharan Africa with an annual growth of 5.7%. This can be attributed to a stable macroeconomic environment, positive investor confidence and a resilient services sector . The Kenyan health system is funded by government revenues, National Health Insurance Fund (NHIF) contributions, private health plans and donations/external funding.

In regard to the medical devices manufacturing and supplies subsector, Kenya is seen as a promising market, having been ranked as the fastest growing market in Sub Saharan Africa Kenya’s medical device market will expand by a five-year compound annual growth rate (CAGR) of 8.9% in local currency terms and 8.2%, which should see it rise to $197.9 million by 2026. The country’s growing health consumption and positioning as the medical tourism destination for its neighbors has created the need for increasing medical devices and supplies in hospitals as well as modernizing the existing ones. Common Market for Eastern and Southern Africa (COMESA) and East African Community (EAC) membership have boosted regional trade with 90% of exports shipped to other African countries. The market has attracted investors and manufacturers due to the tax incentives and the readiness of the government to work with the private sector. Health system reforms are aided by international funding.

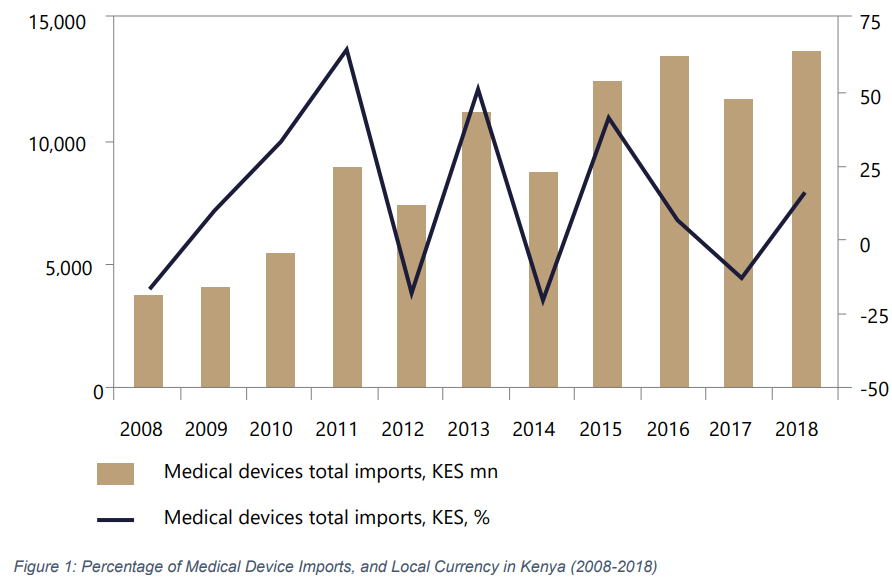

The medical device sector is heavily reliant on imports with limited domestic production due to limited manufacturing infrastructure and technical capacity as well as lack of access to raw materials. The graph below shows the growth of Kenya medical device imports in percentage and local currency. The fluctuation in imports is attributed to changing political landscape and priorities of the government in play.

Kenyan Market Structure

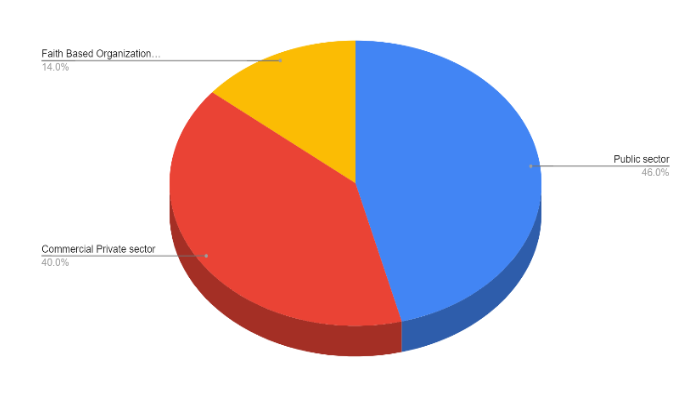

Kenya healthcare market is divided into three subsystems, namely the public sector, the commercial private sector, and the Faith Based Organizations (FBOs). The public sector is the largest in terms of facilities at 46%, followed by commercial private sector at 40% and then the FBOs at 14%. There is a large disparity between these health facilities especially in the rural parts of the country. In the fiscal year 2018/19 the public sector had 43.8% of medical device market share on average. The private sector had 39.0% on average of medical devices market share. FBOs operate in a unique space given their coverage and financial capability, they had 17.2% of medical device market share on average. However, FBOs provide 40% of all commercial private healthcare needs. This means that they have a 40% share of the private market. FBOs are not-for-profit organizations but the commercial aspect of their business is to ensure they make money for them to be sustainable and facilitate the day-to-day running of their facilities.

- Public sector sources medical equipment through the Kenya Medical Supplies Authority (KEMSA). Through specific government programs like the Managed Equipment Services (MES). The public sector is generally regarded as an extremely price sensitive market.

- KEMSA: a state corporation under the Ministry of Health established under the KEMSA Act 2013 whose mandate is to procure, warehouse and distribute drugs and medical supplies for prescribed public health programs, the national strategic stock reserve, prescribed essential health packages and national referral hospitals. All national and local level facilities are by law obliged to first purchase from KEMSA. Only if the items are not available, they are allowed to source their supplies from other private sector distributors.

- Managed Equipment Services (MES): The GOK started the MES project in 2017, with a focus on theater, central sterile services department, renal, ICU and radiology equipment. The MES project is a flexible, long-term contractual arrangement that involves outsourcing the provision of specialized, modern medical technology and equipment to private sector service providers.

- Faith Based Organizations: Comprise of NGOs and other organizations such as the Christian Health Association of Kenya (CHAK), Kenya Conference of Catholic Bishops (KCCB) and the KenyanRed Cross, etc. Most of them have general practitioners with a few being staffed by resident general surgeons or gynecologists. FBOs are mostly involved in primary health care with only a small number offering specialized services. Some big FBOs facilities such as AIC Kijabe Hospital are classified as referral hospitals. A small number of them offer highly specialized services. FBOs source from MEDs on different scales, mostly determined by the Africa Christian Health Association Platform (ACHAP). ACHAP provides the framework for a collaborative network with a cohesive voice to advocate for equitable access to quality health care.

- Mission for Essential Drugs and Supplies (MEDS): a Christian non-profit organization registered as a Trust of KCCB and CHAK. The organization has three main functions: health advisory services, supply chain and distribution, and quality assurance services. MEDS is the first point of purchase for FBO facilities. However, other facilities, both in the private and public sector, can be purchased from MEDS. It is among the 11 recognized international pharmaceutical wholesalers who consistently provide safe, effective and quality essential medicines and other medical commodities. MEDS supplements most of what KEMSA does not have or is unable to procure.

- Commercial Private Sector: The private sector mainly sources for higher-end medical equipment through MEDs. Consumables are normally sourced through KEMSA and MEDs. When the supplies are unavailable or limited, then purchasing is done from other suppliers. While western branded equipment is often considered more advanced and specialized, lower-level private facilities in low resource areas are looking for small scale and easy to use medical equipment. Additionally, the private sector is keen on the maintenance cost, lifetime of the devices, operability, and the purchase cost. However, the current market areas of needs and demands are majorly consumables and other medical devices. Partnerships and collaborations on the supported programs such as maternal and child health services is always a good way to do business with the commercial private sector.

Commercial Distributors: Even though Kenya imports medical equipment from different countries, the largest medical equipment companies that have presence in the country include Philips, GE and Medtronic. Commercial distributors have very efficient and effective infrastructure to market penetration of products. This is based on the fact that they have a well-maintained transport system and communication facilities for running their activities. These distributors are able to have competing products in their portfolio. Other distributors only offer a distribution platform, but the product sales team is responsible for sales. A distribution company can also take care of both. A growing number of medical distribution companies are having a technical team who can handle the servicing of equipment and will provide this to the healthcare facilities.

Overview of the landscape

According to Lusha’s database of private companies classified as medical equipment manufacturing companies in Kenya, there exists 29 companies manufacturing and/or distributing an array of medical equipment in Kenya.

We’ve picked out companies in product categories mainly in consumables, vitals monitoring & diagnostics imaging and other equipment (See Products Section):

Jaza Rift Analysis

Private Sector & FBOs:

- Manufacturers & Assembly: NegusMed (Manufacturing consumables such as bandages and dressings, suturing materials, HopeTech+ (Manufacturing and Assembling Assistive Equipment such as hearing aids, walking sticks, etc.) and Neopenda (Designing and outsourcing production of a vitals monitoring equipment for neonates and grown-ups) are some of the early-stage startups examples. Nexus Medical (Large scale manufacturing and distribution of consumables, obstetrics equipment and hospital furniture) and Revital health (Large-Scale manufacturers of consumables such as syringes).

- Distributors and Wholesalers: Ilara Health (Distributors of easily portable diagnostics equipment from markets outside Africa to clinics and pharmacies from) and Via Global Health (Distributors of an array of medical equipment manufactured both in Africa and abroad) are well known startups in the ecosystem. MEDS, as seen above, is the first point of purchase for FBO facilities. Mediquip Global and Harley’s Ltd are some of the companies distributing medical equipment (varying in size and function) at a larger scale.

Public Sector:

- Manufacturers & Assembly: The Kenyan government currently leverages on the local and international private sector for medical equipment manufacturing. This provides a huge opportunity for Public and Private Partnerships (PPPs). Private sector manufacturers leverage on this as this is evidence for the existence of demand in the market.

- Distributors and Wholesalers: KEMSA and MES as seen above, are GOK owned. All national and local level facilities are by law obliged to first purchase from.

Overview of medical device manufacturing

Medical device manufacturing includes all aspects of the fabrication of a medical device, from designing a manufacturing process to scale-up to ongoing process improvements. It also includes the sterilization and packaging of a device for shipment.

Throughout the manufacturing process, medical device manufacturers strive to be faster and more efficient, but they also wish to be responsible for adhering to protocols and regulations. Thus, manufacturing demands constant insight into renewable resources, sustainable materials, equipment that is more energy efficient, and methods to reduce waste creation. Solutions to these issues can come in the form of improved processes, technological advances in machines or equipment components, or safer/more reliable materials. The same principles apply to the packaging process.

While speed and cost-savings are vital to successful manufacturing, quality control is of the utmost importance — particularly as medical device market demands shift toward a more value-driven landscape. Packaging validation; proving to the regulatory bodies that a product is sterile when it ships, is the final step.

Many medical device manufacturers excel in the ideation, concept, and prototyping phases of product development and outsource the production of components or entire devices to contract manufacturers. This is as true of established original equipment manufacturers (OEMs) as it is for mid-sized companies and startups. Contract manufacturers vary in size and expertise, as well — some comprise small, precise operations specializing in particular materials or components, while others are massive cleanroom facilities equipped for large-scale production.

We aim to undertake a thorough examination of the current landscape of medical equipment manufacturing across different African markets; Kenya being the market of focus. By providing detailed insights into existing products, supplemented with concrete examples, to identify critical gaps in the market where demand for specific equipment surpasses the available supply.

PRODUCTS

Overview

From the onset of the COVID-19 pandemic, Africa has remained among the last in line to access necessary medical supplies and tools—from personal protective equipment and diagnostics to treatments and vaccines. Because there is limited local manufacturing, many countries are reliant on imports, but supply chain disruptions slowed imports and producing countries declined exports to meet their own needs. Additionally, many wealthy countries procured more doses than they could use, leaving little for others with less purchasing power.

These challenges are not new, the pandemic merely highlighted the continent’s long-standing, inequitable access to lifesaving medical products. As a result, concerted efforts are underway to strengthen Africa’s capacity to develop and produce health products that meet its needs.

Several countries in Africa already have capabilities in vaccine and drug manufacturing and fill and finish capacity, that is, the steps that follow production, such as filling syringes, labeling, packaging, and quality inspection. However, there still remains a significant gap to close.

Existing Products

- Diagnostic Imaging Equipment: Leading Kenyan private sector hospital groups invest in the latest most innovative equipment. Best prospects for diagnostic equipment include electrocardiographs (ECG); ultrasound units; scintigraphy apparatus; MRI equipment; angiographies; endoscopies; and biochemistry, hematology, and immunology systems. Hospital groups also invest in radiation equipment including, radiotherapy machines, CT scanners, X-ray machines, and imaging parts and accessories such as contrast media, medical x-ray films, x-ray tubes, and other parts and accessories.

- Dental Equipment: Exporters’ best prospects for dental equipment include dental drills; chairs; and X-ray equipment, instruments, and supplies such as dental cement, teeth, and other fittings, and artificial teeth.

- Orthopedics and Prosthetics: Exporters’ best prospects include fixation devices, artificial joints, and other artificial body parts.

- Patient Aids: These include hearing aids, pacemakers, and therapeutic appliances such as therapeutic respiration apparatus and mechano-therapy apparatus.

- Lab testing equipment: Demand for various rapid diagnostic testing kits will reduce with the reduction of COVID-19 cases in the country. Demand for lab equipment and reagents will remain static. The need for self-testing kits will grow steadily as the government approves licensing for RDTs for malaria, HIV, and COVID-19.

- Consumables: Local production of basic consumables remains low while the demand for them remains the highest out of all the category products. The consumables market includes equipment bandages and dressings, suturing materials, catheters, syringes, surgical gloves, and blood grouping reagents. Nearly 90% of all consumables are imported from China and India.

- Other Medical Equipment: There is market for products to be procured such as hospital furniture, anesthetic machines, anesthetic trolleys, hydraulic operating tables, delivery beds, infant incubators, mortuary trolleys, hydraulic operating tables, mercurial sphygmomanometers, oxygen flow meters, medical & surgical sterilizers, ultraviolet or infra-red ray apparatus, wheelchairs and ophthalmic instruments.

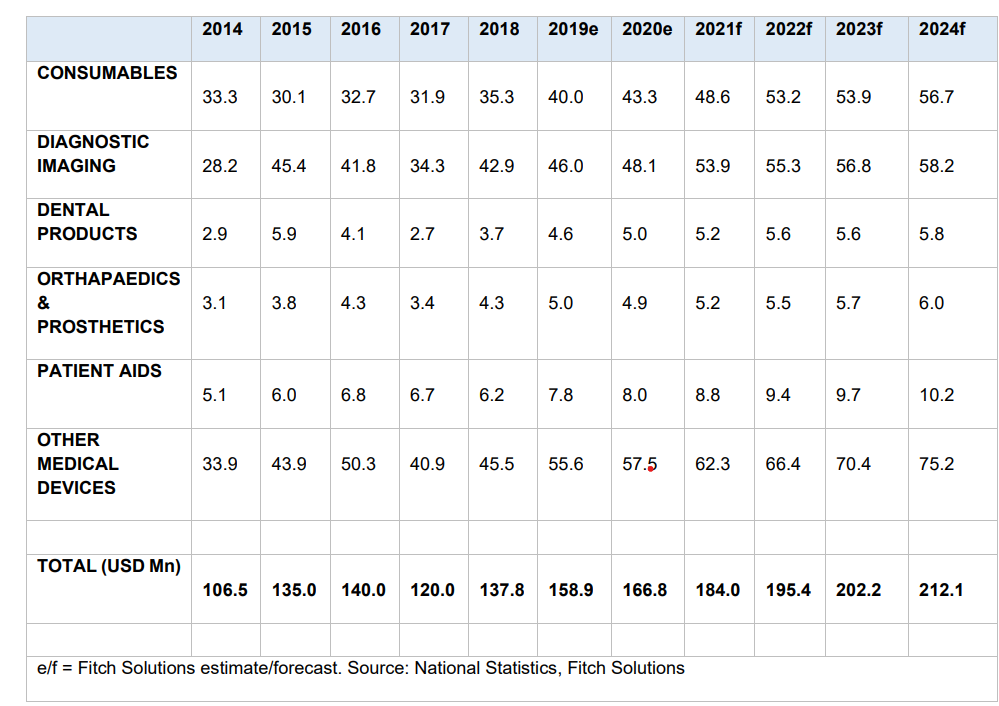

Almost all of the medical equipment is imported from China, India and other countries outside Africa. Below is a summary of medical devices imports from 2016-2026 according to Fitch Solutions.

Medical Equipment Opportunities in Kenya

Organizations with an interest in Kenya typically produce, assemble and deliver medical devices, supplies and/or supply packages (medical kits) for diagnostics, treatments and/or rehabilitation, either high-tech/end or specifically designed or tailored for low resources settings (point of care). Areas of focus in terms of medical specialties include radiology, oncology, cardiology, obstetrics/gynecology, surgery, and neurologic and orthopedic rehabilitation. Following more specific trends in Kenya, the following areas of opportunities (however, not limited to these):

- Obstetrics: Neonatal disorders are the third largest cause of death in Kenya, especially in lower resource communities. The Free Maternal Service (FMS) policy was introduced in Kenya in 2013. This has increased utilization of the skilled birth attendant among the women who dwell close to the hospitals and who could not afford for the services initially. However, there still exists a challenge to the utilization of FMS among the poor women in remote areas.

- Cardiology: Cardiovascular diseases are responsible for much of the growing Non-Communicable Diseases burden in Kenya. Estimates show that 25% of hospital admissions and 13% of deaths in Kenya are due to cardiovascular diseases. In 2018, Kenya launched the national cardiovascular disease management guidelines, and it is argued that related specialty services and solutions will grow in the near future. It is expected that opportunities will arise both in the installed base as well as new installments. There is also an urgent need for palliative care due to the current late-stage diagnosis of cancers (survival rate below 10%). Screening program solutions for earlier detection is also an area of opportunity.

- Oncology: An increase in the number of cancer cases in Kenya over the past decade resulted in legislative actions and policies to guide delivery of cancer services. Kenya’s recently launched National Cancer Control Strategy and past policy efforts provide an opportunity to synergize information and enhance understanding to improve cancer diagnosis and treatment in the country.

- Radiology: It is expected that radiology services for diagnostic imaging, therapeutics and image guided procedures will grow in Kenya. According to the Society of Radiography Kenya (SORK), there are approximately 1,070 registered radiographers in Kenya, which is estimated to be more than 90% of the diagnostic and therapeutic radiographers in Kenya. Over half of the MRI and CT scan machines are operated by the private sector. Until 2017, there was no nuclear medicine, mammography and radiotherapy equipment available in the private sector.

- Trauma and Critical Care: The growth and development of trauma and critical care in Kenya has largely been as a result of the efforts of anesthetists and international partnerships. Strengthening of Intensive Care Units (ICUs) is a focus under the MES project. The COVID-19 pandemic highlighted the importance of intensive care specialists in Kenya. Solutions for early (mobile) diagnostics and real-time guidance for trauma are mentioned as a niche market, especially in the light of heavy traffic in cities and distance to hospitals in more remote areas.

Regardless of the areas of opportunities mentioned above, we believe there’s tremendous opportunity in the medical manufacturing industry as a whole regardless of the area of medical specialty as most African countries, including Kenya, import 80% and above in volume of every category of medical equipment. Hence, there’s a high demand for local medical equipment manufacturing, thus, more private sector players ought to tap into the existing demand.

Factoring in the information on the market demand and opportunities, we can see that regardless of the medical specialty, the need to localize manufacturing supersedes that as 70% of all medical devices within the African market are imported.

With that said however, most demand for imports and local manufactured devices is concentrated on consumables such as bandages and dressings, suturing materials, catheters, syringes, surgical gloves, and blood grouping reagents and other equipment such as oxygen flow meters, medical & surgical sterilizers, ultraviolet or infra-red ray apparatus, etc.

Below is further assessment of the types of products recommended as ones to prioritize due to the high demand as they are consistently used in the patient care journey.

Syringes Market

The global syringe and needle market was valued at US$ 5.1Bn in 2023 and is expected to increase over the forecast period at a CAGR OF 1.3% to reach US$ 5.6Bn in 2030. While for the MEA region, the syringes market is estimated to be worth US$2.15Bn by 2028, growing from US$ 1.61Bn in 2023 at a CAGR of 5.98%.

Africa’s population growth and routine childhood immunization needs, accounted for the highest demand for syringes in the continent. That all changed with COVID-19 vaccines. Suddenly, demand for syringes skyrocketed. Meanwhile, the need for routine immunizations—for diseases such as measles, whooping cough, polio, and more—didn’t stop.

In July 2023, Revital Healthcare became the first-ever African manufacturer approved by the WHO to produce early activation auto-disable syringes—a milestone that will help diversify the geographic supplier base of syringes and strengthen manufacturing capacity in Africa, allowing for rapid and sustainable vaccine delivery on the continent.

Syringes can be classified in 3 categories:

- By Useability: Sterilizable/Reusable syringes, Hypodermic syringes, Disposable syringes, Conventional syringes, Safety syringes (Retractable and Non-Retractable) and Prefilled syringes.

- By Material: Glass and Plastic syringes.

- By Type: General syringes, Specialized syringes (Insulin, Tuberculin, Allergy syringes), Other syringes (Angiographic and Catheter syringes).

Competitive Landscape

On a global scale, the syringe market is dominated by a couple of players. Top 3 competitors include:

- Becton Dickinson (BD) (US): They dominate the market with hospitals as the primary client with over half of total sales. They have extensive production capacity thus they are able to provide products at competitive prices. Sales of their Hypodermic needles, Injection needles and Retractable syringes enables them to secure the top spot

- Cardinal Health: Their acquisition of Medtronic’s Patient Care division helped them cement their market position. They excel in production of safety syringes.

- B. Braun (US): With substantial growth of their sales being in Europe, their major product lines include standard and fine-dose 2-part and 3-part syringes.

- Others: Terumo Corporation (Japan), Smiths Medical (US), NIPRO Corporation (Japan), Hindustan Syringes and Medical Devices Ltd. (India), Gerresheimer AG (Germany), SCHOTT AG (Germany) are some of the other players in the market.

Wound Care Market

The global wound care market is estimated to grow from US$ 7Bn in 2020 to US$ 11.2Bn by 2025 growing at a CAGR of 7.9%. The market size of the traditional wound care (gauze, bandages and tapes) industry in Kenya is expected to rise by USD 3.0 million with a CAGR of 7.2% by the end of 2028. The growth of the market is attested to the growing number of road accidents, increasing cases of chronic, surgical and traumatic wounds, high rate of cesarean births, rising cases of burn injuries and technological advancement in wound dressings.

Most sales are made to hospitals, clinics and retail channels such as supermarkets, pharmacies, etc.

Wound dressings products are classified according to:

- Type of product: Traditional vs Advanced wound dressings

- Traditional wound dressings comprise of adhesive bandages, first aid kits, and gauze pads & tapes

- Advanced wound dressings comprises Form dressings (Silicon and Non-Silicone), Hydrocolloid, Hydro fiber, Film, Alginate, Collagen, Hydrogel, Wound contact, Superabsorbent, etc.

- Application: Surgical and Traumatic wounds, Diabetic foot ulcers, Pressure ulcers, Venous Leg ulcers, Burns, etc.

- End user: Hospitals and clinics, ambulatory care and home-based care.

Competitive Landscape

In Kenya, the traditional wound care market is dominated by key players, like Ray Pharmaceuticals Ltd, Yibin Hengkang Industrial Co. Ltd., Beiersdorf AG, Mercury Group of Companies.

Globally, the major players operating in the global medical tapes and bandages industry include Mölnlycke Health Care AB, Smith & Nephew PLC, Ethicon Inc., Medtronic, 3M, Beiersdorf AG, Urgo Medical, Dynarex Corporation, Winner Medical Group, Inc., McKesson Corporation, Cardinal Health, 3L Medicinal Products Group, B. Braun Melsungen AG, Paul Hartmann AG among others.

3M is the leading company in the global wound dressing market. 3M is a pioneer in advanced wound care and has been in the market for more than 15 years. They are focusing to increase their market share by expanding to untapped emerging markets, Africa being one of the markets for expansion.

Surgical Gloves Market

The medical gloves market, which was valued at USD 16.9 billion in 2022, would rise to USD 36.82 billion by 2030 and is expected to undergo a CAGR of 10.20% during the forecast period 2023 to 2030. While the Middle East and Africa protective gloves market is expected to gain market growth in the forecast period of 2021 to 2028. The market is growing at a CAGR of 6.4% in the forecast period of 2021 to 2028 and expected to reach USD 1.5 Bn by 2028.

Surgical gloves are widely used by healthcare professionals while performing surgical procedures, which assists to reduce the transmission of infection from patients to healthcare professionals. The demand-supply gap for surgical gloves is expected to expand internationally due to supply restrictions including limited manufacturing capacity and lengthy construction time.

The market is categorized according to:

- Product Type: Examination, Surgical and Chemotherapy.

- Sterility: Sterile Gloves and Non-sterile Gloves.

- Form Type: Powdered Form and Powdered-free.

- Raw Material Type: Latex, Nitrile Rubber, Vinyl Rubber and Polyisoprene.

- Usage Type: Disposable, Reusable and Others.

- Distribution Channel: Direct Selling, Medical Store, Online and Others.

- End User: Hospitals, Clinics, Ambulatory Surgery Centers, Diagnostic Centers, Rehabilitation Centers and Others.

The opportunities that will be contributing to the growth of the market include the demand for chemotherapy which is anticipated to increase because of the increasing cancer incidences. With the growing demand for chemotherapy, the demand for chemotherapy-grade gloves is also anticipated to increase.

The increasing prevalence of chronic diseases has also surged the number of hospital visits and re-admissions, which is, in a way, positively impacting the product demand globally.

There is a high chance of infection after the use of medical gloves. Numerous adverse skin reactions, including allergic contact dermatitis, irritant contact dermatitis, and contact urticaria, have been witnessed with these gloves. Wearing gloves for prolonged periods also causes moisture to build up, eventually increasing the risk of fungal infections. Thus, this factor hampers the market growth.

Competitive Landscape

Some of the major players operating in the medical gloves market are: Cardinal Health. (U.S.), Medline Industries, Inc. (U.S.), YTY Group. (Malaysia), Arista Networks, Inc. (U.S.), JIANGSU JAYSUN GLOVE CO., LTD (China), Bluesail Medical Co., Ltd. (China), Shandong Yuyuan Latex Gloves Co., Ltd. (China), Zhanjiang Jiali Glove Products Co., Ltd. (China), McKesson Corporation (U.S.), Dynarex Corporation. (U.S.), Robinson Healthcare (U.K.), SHIELD Scientific B.V. (Netherlands), 3M (US), PAUL HARTMANN AG (Germany) and other players both local and global.

DISTRIBUTION CHANNELS

Supply chain infrastructure for distribution of medical devices is still under development in most African countries. However, due to technology revolutionizing supply chain, more local players are filling in the missing gaps in supply chain inefficiencies.

Most international and local manufacturers have their own sales teams operating internally and externally while setting up partnerships with public and private sector players. Organically, the teams sell their products directly to the hospitals and clinics, wholesale distributors and/or retail distributors. Their sales teams work utilizes both online channels (website) and offline channels (consisting of physical locations like warehouses and/or retail stores).

A very effective channel used by manufacturers to penetrate the market and increase sales is the utilization of both public sector distributors (KEMSA, MEDS, etc.) and privately owned commercial distributors, who leverage their efficient and effective infrastructure to market penetration of products. A growing number of medical distribution companies have a technical team who can handle the servicing of equipment and will provide this to the healthcare facilities in their CRM database. This saves the medical device suppliers resources to go to market.

Next in the Medtech series, tune in for a collaboration article with our conveyor belt partner, Villgro Africa, on the learnings shared from 2024’s Transforming Africa Medtech Conference that took place in Nairobi, Kenya on the 28th to 30th of August.